carolmusyoka consultancy

carolmusyoka consultancy

@carolmusyoka

@carolmusyoka

Yet another Benchmark Lending Rate

A father who is very concerned about his son’s bad grades in math decides to register him at a catholic school. After his first term there, the son brings home his report card: He is getting “A”s in math. The father is, of course, pleased, but wants to know: “Why are your math grades suddenly so good?” “You know”, the son explains, “when I walked into the classroom the first day, and I saw that guy on the wall nailed to a plus sign, I knew one thing: This place means business!”

The Central Bank of Kenya (CBK) last week set the first pricing of the Kenya Banks’ Reference Rate (KBRR) placing it at 9.13%. The media followed with the usual tantalizing lead-in headlines: “Loan pricing set to come down in Kenya” and “Cheaper loans for Kenyans”. Our roads started to shudder in collective trepidation at the mere thought that more cars would trudge a traffic laden path, as cheaper loans mean more Kenyans would flock to roadside dealerships to buy the ultimate sign of prosperity – a reconditioned car. Last week’s announcement of (yet another) government attempt to bring down the cost of borrowing was met with the typical enthusiasm that cheap credit starved Kenyans reserve for any sign of relief.

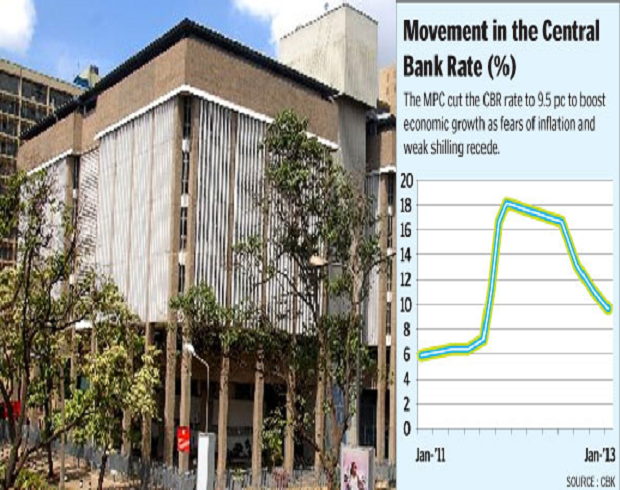

The Central Bank began flogging this non-starter of a rate setting horse back in June 2006 when they launched the Central Bank Rate (CBR) at the rate of 9.75%. One of the objectives for the CBR was to create a transparent mechanism for commercial banks to set a base rate for their commercial loans. An independent body – the Monetary Policy Committee of the CBK – would set a rate that was reflective of the Kenya shilling rather than the profit motivated banks that were never quite transparent in how they arrived at the amorphous base rate. But commercial banks ignored it and continued to set their own base rates. After all there was neither an implicit nor explicit consequence for not using the rate. The CBR has garnered more success in reducing volatility of short-term interest rates particularly in the interbank lending rate space.

According to CBK data, commercial bank average lending rates moved from a high of 18.13% in January 2013 to 16.99% in December 2013. However, your average retail borrower does not enjoy these rates since about 60% of commercial bank lending in value terms sits in the large and medium corporate space and these borrowers are able to negotiate personalized rates for their corporate loan books. These ‘personalized’ rates are based primarily on their borrowing and repayment history, strength of their balance sheet, income statements and cash flows, majority shareholding ownership, as well as ability to make loan repayments in the future. In essence it is a specific internal credit rating that will guide the pricing for these corporate entities and will ensure that their perceived risk premium is uniquely priced. The rest of the “watus ” borrow at bank base rates plus a standard premium. That standard premium does not in any way differentiate between a new borrower or one who is borrowing his fifth or sixth unsecured loan and who has faithfully repaid his loan, or perhaps even prepaid some of his loans, in good time.

The role of the Credit Reference Bureaus (CRB) thus becomes critical in ensuring that such differentiation lowers the price of loans to the good consumer. However, the CRBs were initially set up to allow for information flow regarding bad bank customers who didn’t repay their loans, wrote bouncing cheques or failed to fund their accounts on time leading to debit balances due to overdrawn accounts. The Treasury Cabinet Secretary Henry Rotich apparently gazetted rules earlier this year requiring the sharing of positive information by the banks to CRBs. It’s about time. The bigger and more effective step is to require the banks to use credit rating history on individuals and institutions to arrive at the risk premium above which the banks will price customer loans. Setting a new base rate for banks to price loans is like putting lipstick on a pig. It remains a pig nonetheless. Fact: 12+9 is also equal to 20+1. The difference in the above equations is the same and that’s the lipstick on the pig.

What the government and the samosa-munching “Taskforce To Reduce Interest Rates” brigade need to do is to get Kenyan commercial banks to price on differentiation. The banks should be able to demonstrate to the CBK banking supervision chaps that retail customer A’s loan pricing is benchmark rate + risk premium where that risk premium is calculated as that appertaining to a specific credit rating.

But perhaps that’s just too much admin. Differentiation of customers means that the bank can’t benefit from the upside of standard pricing that captures the good borrowers and the bad. The standard pricing enables the bank to hide its inefficiency in controlling bad loans by having a blanket rate that will ensure good loans cover and bring in the profitability that the bad loans are dragging down. The retail loans are managed on a portfolio basis rather than on an individualized basis allowing for the bad apples to be covered by the sweat and blood of the good ones.

By driving a differentiated pricing agenda, the Central Bank will ensure not only actual lowered credit pricing for consumers including better uptake on mortgages, but it will also drive a more disciplined approach to bank account management by the Kenyan banking consumer wishing to build a positive credit rating for their future borrowing. Creating yet another benchmark rate is playing with numbers. No matter how low you set the give-it-whatever-name-you-want benchmark rate, the premium above it is what will determine if the true cost of credit is coming down. Currently the CBK has no control over that. Driving a differentiation agenda is the nail on the proverbial cross that we need.

[email protected]

Twitter: @carolmusyoka